FINANCIAL PLANNING

Financial planning is the process of pursuing your life goals through proper management of your finances. This can help you to enjoy your life today, knowing you have taken care of tomorrow.

Life goals can include buying a home, saving for your child's education, retirement or legacy planning. The easiest path to financial freedom in achieving these goals is through preparation. Yet, adequately preparing for your future can be an arduous journey because most people do not have the training, expertise, experience, research or tools. Indeed, this vital task in our lives can be intimidating. Let us help you.

This six-step process can help you make sense out of all the micro components by taking a look at the "big picture" of where you are financially, what you may need in the future and what you must do to reach your goals.

BENEFITS OF FINANCIAL PLANNING

Financial planning provides direction and meaning to your financial decisions by helping you understand how each decision affects other areas of your finances by considering its short and long-term effects on your life goals. It helps you with opportunity cost decisions since often electing one choice means forgoing another. By prioritizing your needs, it can help ensure that the most important things are taken care of first.

There are psychological benefits to financial planning since financial planning can help clarify where you are now, where you want to be and identifies the actions steps to help you get there. It also allows you to adapt more easily to expected and unexpected changes in your life and can help you feel more secure knowing that your goals are on track. Taking proactive action steps to provide for your own and loved ones' financial security can provide you with clarity by helping you confront risks such as dying too soon or living too long.

Lastly and probably most importantly, financial planning can help provide equilibrium in your life since it helps you live life today knowing you have taken care of your life tomorrow.

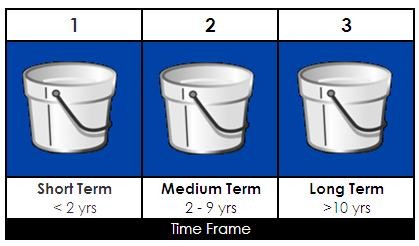

THE THREE BUCKETS

We believe that “proper management for your finances” means charting the most optimal path using strategies that increase your cash-flow, reduce your taxes and that create & protect your wealth. This often involves aligning your goals into three categories: short, medium and long-term.

Quantifying your goals in this manner, allows you to align your finances and investments accordingly into three buckets and allows you to optimize the returns, risk, taxation, liquidity, investment flexibility, product fees and platforms used.

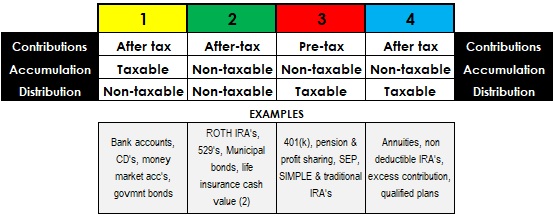

THE FOUR TAX WINDOWS

The impact of taxation on your contributions, your accumulation and when you take distributions can have a profound impact on your results and should not be ignored. The three primary types of taxation you need to be concerned about are income tax, capital gains tax and estate or gifting taxes.

A carefully thought out financial plan will attempt to align your three buckets (above) with the most appropriate tax window for your envisaged current and future circumstances. This means taking cognizance of the tax consequences of your contributions, accumulation and eventual distribution of assets as per the following table.

NOTE:

1) The information provided is based on our general understanding of federal income taxation and is for illustrative purposes only. Since we do not give tax advice, we recommend that you obtain such advice from your tax adviser related to your specific situation.

2) Under current Federal tax rules, you generally may take income tax-free withdrawals under a permanent life insurance policy which is not a modified endowment contract up to your basis in the contract. Loans taken will be free of current income tax as long as the current policy remains in effect until the insured's death, does not lapse or mature, and is not a modified endowment contract. This assumes the loan will eventually be satisfied from income tax-free death proceeds. Loans and withdrawals reduce the policy's cash value + death benefit and increase the chance that the policy may lapse. If the policy does lapse, mature or become a modified endowment, the loan balance at such time would generally be viewed as distributed and taxable under the general rules for distributions of policy cash values.

YOU MIGHT ALSO BE INTERESTED IN: